Information Specific to Foreign Investors

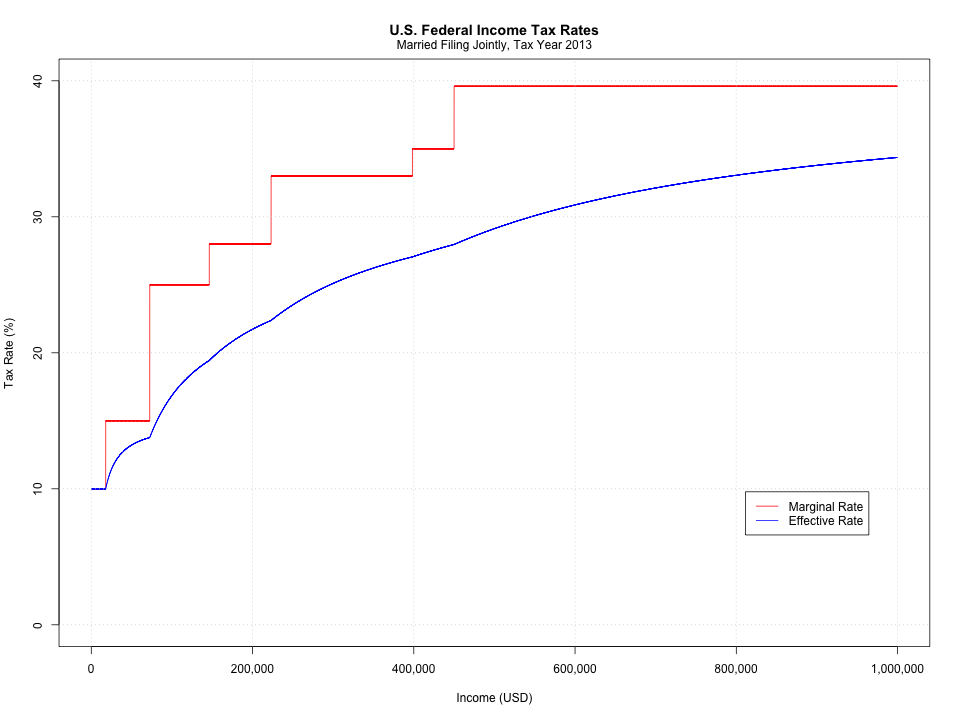

A Non Resident Alien (NRA) owning property in the US pays local tax but still does not have to file an income tax return with the IRS. The default regime is 30% withholding of all gross payments. However, the taxpayer can elect for the same treatment as US taxpayers in which case tax are due on net income instead of gross income. This is called the election for Effectively Connected Income (ECI) treatment.

US Classification of income into FDAP and ECI for Non Resident Alien

The IRS classifies income into two general categories:

- The Fixed,-Determinable,-Annual,-Periodical-(FDAP)-Income. This class of income is subject to a high flat tax rate. It does not allow for any netting of related expense, FDAP applies on stock dividends, bond coupons and US savings account interest.

- The Effectively-Connected-Income-(ECI)), meaning connected to some business or activity in the US. ECI is subject to gradual income tax on the basis of US based net income. The important difference it makes for investor is only taxed on Net Income.

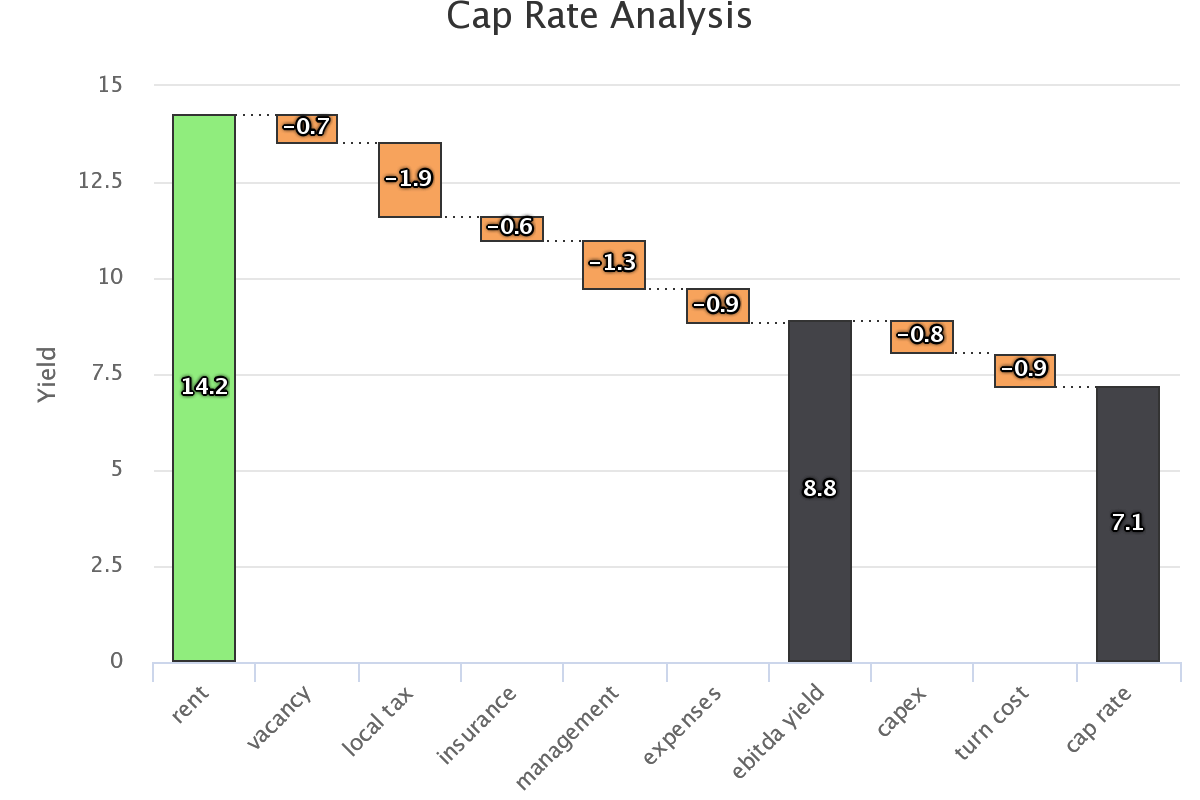

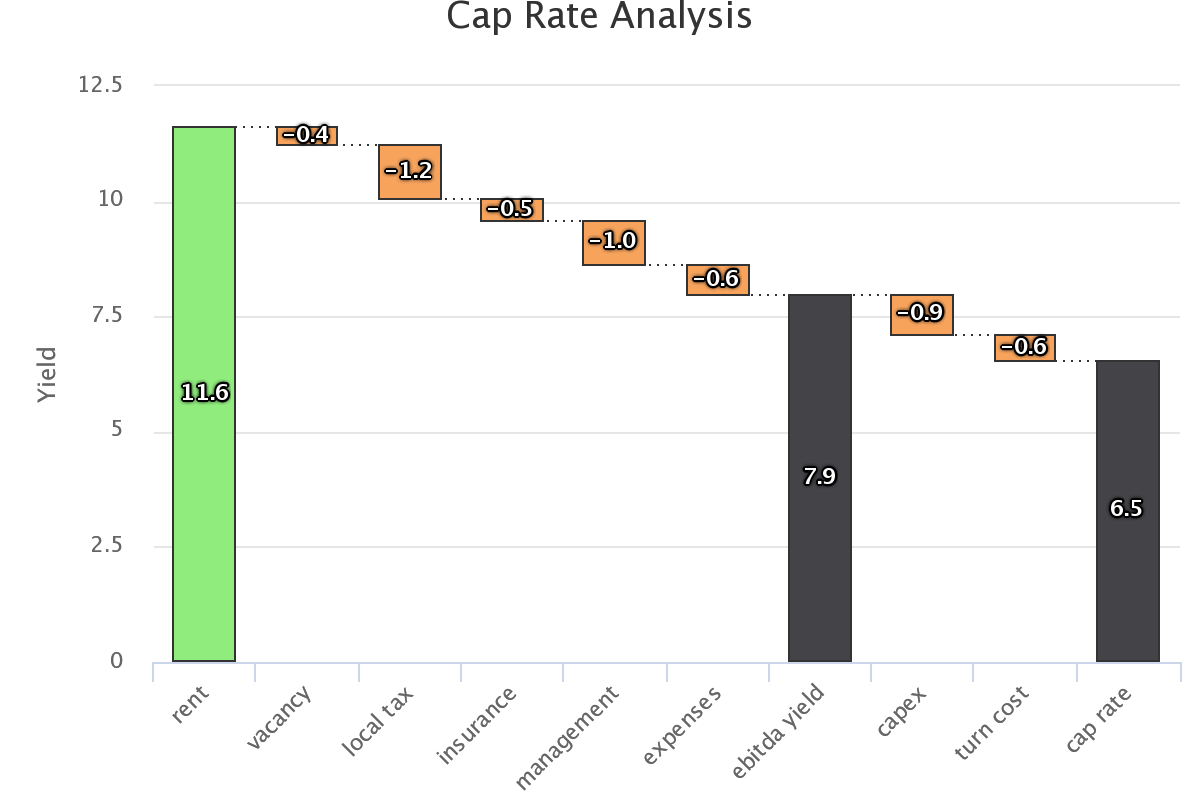

The ECI treatment allows for deduction of all expenses related to the investment, including mortgage interests, local taxes, insurance, repairs, property management, etc. NRA who own real estate directly and supports these costs can and should elect for ECI treatment. Not doing so would result in the property expenses not being offset against income, and the gross income being taxed at a high flat rates of 30%. A consequence of opting for ECI treatment which is the same advantageous treatment that US investors get, is that the NRA must file US income taxes with the IRS every year.

The election of ECI treatment is done by submitting an election with the tax return (US tax code 871(d)). To avoid withholding of 30%, the alien needs to submit a W8ECI form to his a property manager. He will require this before he distributes any of the rents to the owner, as he is registered as a withholding agent with the IRS. The NRA will need to fill a W8ECI form and send it to his property manager, whereas a US resident is required to file a W9 form.

Once the election is done, NRA should go through the initial setup and registration with IRS.

Initial Setup and Registration with the US Tax Authorities

While all US residents are identified by their social security number (SSN), NRA need to obtain an Individual Tax Identification Number (ITIN) from the Inland Revenue Service (IRS). Obtaining an ITIN will allow to avoid susbtantial withholding tax on rental income and withholding on sales proceeds.

The ITIN can be obtained using a W7 form, which is filled using these instructions.

The IRS charges nothing to give an ITIN to a NRA. Some people will ask $75 to $100 to fill it, You can print the form yourself, fill it with your personal details and send it so you know what you sent and when it was posted, and you'll receive the IRS answer.

- if you are in a country with tax treaty, you can file the W7 with case a

- if there is no tax treaty, you can file the W7 case b with when filing for tax the year after you bought the house. This means you can not get a mortgage..

- to be able to get a mortgage in US, instead of waiting for one year, you can file the W7 case h: mortgage for property investment, attach a enclose a letter from a mortgage provider that says you need an ITIN to get a mortgage.

The elephant in the room: how your domestic jurisdiction treats US income

Some tax jurisdiction (Hong Kong for example) apply territorial taxation, which means that only domestically sourced income is considered for tax. Some others (France for example) apply taxation on global income.

Some double taxation treaty only insuring there is no double taxation (you still pay the highest possible tax), for others you only pay tax in the US.

In the case of France, owning houses directly or through a fiscally transparent LLC results in your having to maintain a set of accounts for the IRS, but then, given the DTT, you do not need another set of account for the french tax authority, following french rental income rules. You still need to adjust the french income by the US declared income for the computation of the effective tax rate, and still are liable to french tax on real estate wealth based on worldwide assets.

This means that it makes sense to own directly a house from Hong Kong, whereas owning a property for a french beneficiary is best done through an opaque entity (i.e., an entity that has its own accounts and files for tax separately).

Advanced Tax Planning Resources

These link direct you to third party websites and documents:

- US Tax Guide for Aliens, document from the IRS, supposed ot be introductory, but reading does not flow.

- NRA Tax Guide similar information, with a conveniently formatted list of tax treaties rates p25.

- Foreign person investing in US real estate a presentation for the American Bar Association, much deeper content (copied in 2016).

- Portfolio Interest can be exempted from tax under certain conditions

- US Tax Code Section 871 rules on contingent interest

- AFR: Applicable Federal Rates

- Davis Malm Guide written in 2019 and updated following TCJA tax reform and makes corporate ownership more attractive to NRA.

Estate Tax

If you are about to die, owning US real estate directly will expose your heirs to high estate tax, with a $60k exemption for NRA instead of $11m for US persons, some estate planning is necessary.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}