Types of Mortgages

We give below an overview of financing options for buy and hold real estate investors.

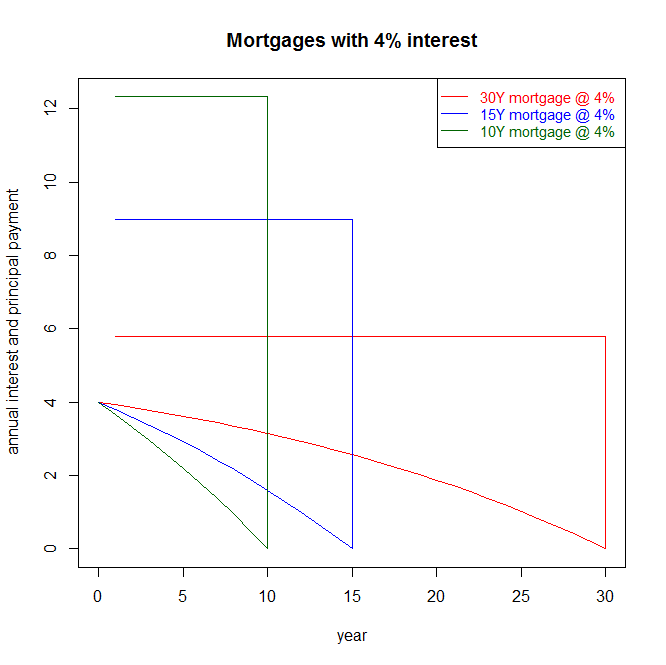

Conforming Mortgages: The Best Deal in Town

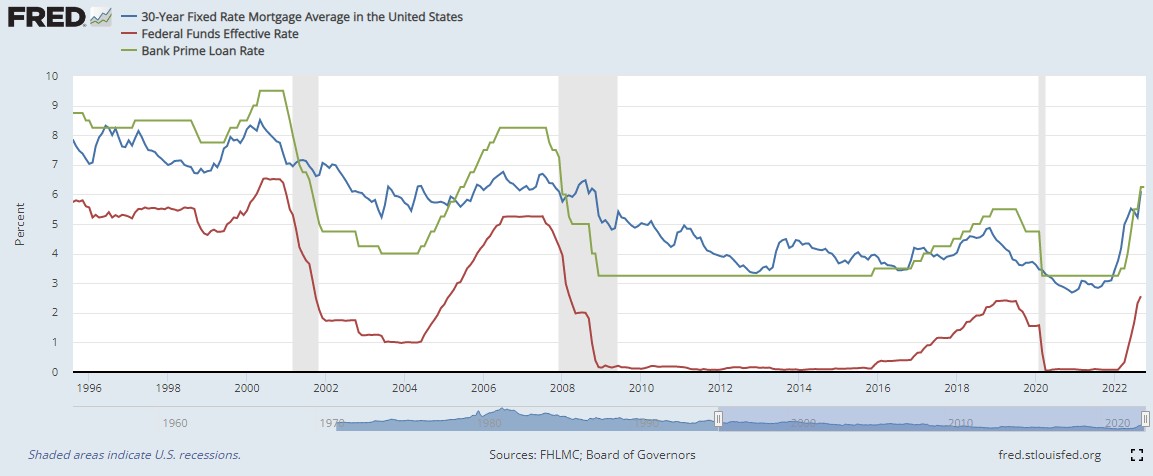

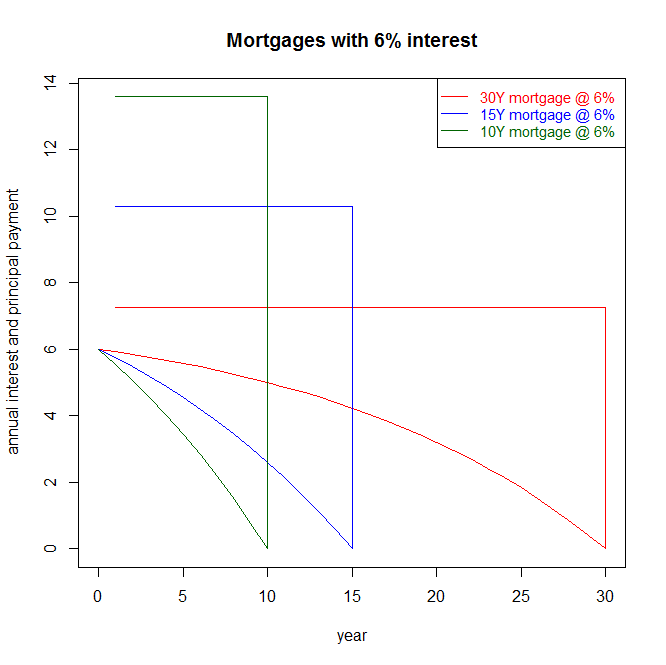

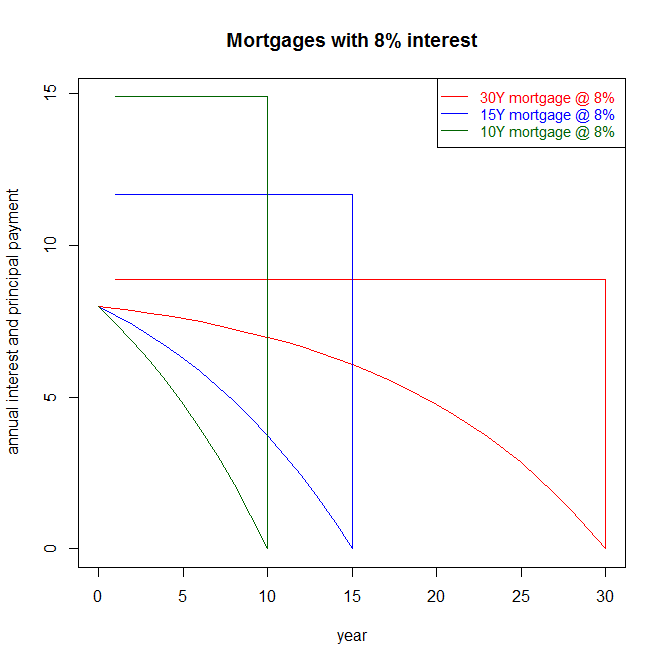

For those who qualify, the so called conforming mortgage might well be the best game in town in terms of low rates and low risks. Such mortgages last for 30 years with a very competitive low fixed rate. They can even be paid back early in case the owner wants to refinance when rates go down.

As bank liabilities have much shorter term, there is significant systemic risk for banks in lending people at fixed rates on such long maturities. Letting borrowers refinance at any time gives further increases the risk, where the lender stands to loose a lot if rates go up, and not gain at all if rates go down.

For the purpose of helping owners get much better deals on their mortgages without bankrupting the banks, the US government sponsored agencies (GSE) that buy back conforming mortgages from banks and have come to dominate the mortgage market.

Those agency policies are ultimately controlled by politicians. In an impressive display of bipartisan consensus, republican President H W Bush signed the Housing and Community Development Act of 1992, the Democratic Congress' view that the GSEs "have an affirmative obligation to facilitate the financing of affordable housing for low- and moderate-income families in a manner consistent with their overall public purposes, while maintaining a strong financial condition and a reasonable economic return."

For this reason, GSE compliant mortgages provide unbeatable rates and conditions.

Portfolio Lending

If your investment does not comply with GSE conditions, you may still get financing. However, lender may offer lower LTV, and floating rate payments after a few fixed years. You may find a portfolio lender by speaking with several mortgage brokers, or investors with similar investments to the one you are looking at.

As a foreigner, I was able to obtain a 5.5% for 5Y (then floating) rate 30Y US based mortgage with 50% LTV. The question in that case is after 5Y, you may have to repay the mortgage because the rates have become much higher, this does significantly adds to your risk.

Collateralised Lending

Even when the investor has sufficient funds to purchase cash, it appears that a reasonable mortgage interest deduction (comparable to the deduction obtained by people who would use financing) can be generated by structuring the investment appropriately.

As a general rule however, you should not be able to deduct more than what an investor would deduct with financing at arm's length. The IRS created many rules intended to avoid abuse, and you may want to check your setup with a professional experienced on such matters.

Foreigners may pay mortgage such interest with no tax by taking advantage of portfolio interest provisions voted by congress or advantageous tax treaties with countries such as Ireland.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}